Consider an Adjustable Rate

With fixed rate mortgages as low as they are, most purchasers or owners wanting to refinance might not even consider an adjustable rate loan. The determining factor should be how long the person plans to be in the home and which mortgage will provide the cheapest cost of housing.

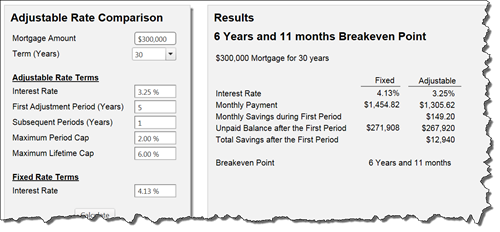

For instance, if you compare a $300,000, 30 year term mortgage with a 4.125% rate on the fixed and a 3.25% on the 5/1 adjustable, the breakeven point would be almost seven years assuming the rates adjusted the maximum that they could in each year.

Therefore, if a person is going to stay in the house less than 7 years, the ARM would provide the cheapest cost of housing. This example shows that at the end of five years, the ARM would generate almost $13,000 savings over the fixed-rate.

On the other hand, this could be a good time for homeowners with an existing adjustable rate mortgage to consider refinancing into a fixed-rate mortgage. The longer that they intend to stay in their home, the more advantageous it might be for them to convert their mortgage to lock-in their payment and fix their housing costs.

A trusted mortgage professional can analyze the alternatives to provide you with the information necessary to make a good decision. You can try the Adjustable Rate Comparison with your own numbers to see the effect.